Article Summary

The operating income formula — Revenue minus operating expenses like COGS, wages, and depreciation — measures a business's core profitability. This article explains the formula, what to exclude (taxes, interest), and walks through a real calculation. You'll gain the clarity to apply and interpret operating income with confidence.

The operating income formula can tell you how profitable and efficient your business is, and the formula itself is so easy an eight-year-old could figure it out. The catch is that the formula is only as accurate as your ledger; solid accounting is essential, as only this will allow the operating income formula to produce solid numbers.

The operating income formula can tell you how profitable and efficient your business is, and the formula itself is so easy an eight-year-old could figure it out. The catch is that the formula is only as accurate as your ledger; solid accounting is essential, as only this will allow the operating income formula to produce solid numbers.

Below we look at how to use the operating income formula and the specifics about why it’s so important. If you find your business is struggling with revenue or efficiency, learn proven strategies to increase leads and sales with this top-rated course on building a profitable business network.

What The Formula Does

Let’s look at a modern example of the basic function of the formula. This article published by the New York Times on the fourth quarter earnings of Netflix provides some very interesting numbers. The numbers we are concerned with are revenue and profits. Netflix’s revenue in the fourth quarter of 2013 was $1.18 billion. Needless to say, that’s a staggering amount of money. But when you subtract all the expenses of running Netflix in the fourth quarter, the profit is a much less eye-popping number: $48 million. In other words, Netflix’s profit was only 4.06% of its revenue.

The Formula basically starts with a company’s figure for revenue and strips it down to pure profitability. This way you (the business owner) and any investors are not mislead by a large revenue.

The Operating Income Formula

Now that you know what the formula does, you could probably construct it yourself. This is the basic version of the operating income formula:

Operating Income = Revenue – (Cost of Goods Sold (COGS) + Wages + Depreciation + other applicable expenses (daily cost of running the business))

It’s important to note that you don’t just subtract every single thing that costs the company money or that appears in the ledger. For example, items that are not subtracted from revenue include interest expenses, taxes, accounting adjustments and pretty much anything else that is not an inherent part of a business’s structure.

The Formula In Action

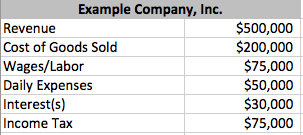

Take a look at the following statement. Obviously a formally correct statement would not look like this, but what’s really important here are numbers, not formalities (gain a better understanding of the uses of income statements with this great post on statement examples and tips):

Now, the first number we want to generate is simply the operating income. From what I mentioned above, we know that to do this we will subtract everything from revenue except the Interest(s) and Income Tax expenses. So:

Operating Income = $500,000 – ($200,000 + $75,000 + $50,000)

Operating Income = $175,000

This is an excellent operating income as it produces an operating margin (the percent-change from revenue to operating income; in this case: $175,000 / $500,000) of 35%. That’s a sight better than Netflix’s 4% profit margin. Start making your own operating calculations (and making them accurately) with this five-star introductory financial accounting program.

However, any business owner would be nagged by the fact that Interest(s) and Income Tax expenses still have to be subtracted at some point. If we go ahead and subtract these two numbers we get our Net Income. In this case, our net income is $70,000. While this is a good measure of what you’ll actually be “left with” when it’s all said and done, there are several reasons that net income is often less ideal than operating income.

Why It’s Important

The operating income formula is important because of the fact that it excludes Interest(s) and Income Taxes, among other things. What the formula is really trying to achieve is a measure of a company’s most important operations: revenue and expenses. Interest, taxes, etc. apply to all businesses and vary accordingly. By excluding these, the formula is able to compare a company by its own unique numbers and therefore provide a certain measure of efficiency, especially when compared to competing companies or to different years in the company’s past. For example, it would be interesting to look at operating efficiency in the years 2005-2010, as a company endures the financial crisis. This would also provide an opportunity to see how the company is managed and how its operating income adapts to drastic, unexpected change.

Obviously, a larger relative operating income is better. Even if you’re dealing with terrible interest expenses, you can see a company’s potential if it has a high operating margin. But like I said earlier, this was a very simplified example and, after all, it hinges on the accuracy of your accounting. If you want to learn a visionary way to reveal the meaning trapped in your financial spreadsheets, check out this class on Understanding Your Business.