Article Summary

Cost allocation methods are management accounting tools that distribute overhead and service department costs—like HR and maintenance—across products to reveal true pricing. This article covers the direct method and step-down method, with worked examples. You'll gain a clear understanding of how each approach affects cost accuracy and profitability.

Keeping track of costs is an essential part of running a business. Cost allocation methods are generally used as a management accounting tool to help to get an accurate idea of the costs associated with various departments within an organization. Proper cost allocation is an essential element in ensuring that organizations are run efficiently and cost effectively. Allocating the costs associated with various service departments within an organization allows management to create a clear idea of the actual cost their services or products. Actual costs are essential for creating accurate accounts to enable the proper billing of clients. Your Business by the Numbers course provides students with excellent training on how to keep track of sales, how to monitor costs, and how to make a profit.

Keeping track of costs is an essential part of running a business. Cost allocation methods are generally used as a management accounting tool to help to get an accurate idea of the costs associated with various departments within an organization. Proper cost allocation is an essential element in ensuring that organizations are run efficiently and cost effectively. Allocating the costs associated with various service departments within an organization allows management to create a clear idea of the actual cost their services or products. Actual costs are essential for creating accurate accounts to enable the proper billing of clients. Your Business by the Numbers course provides students with excellent training on how to keep track of sales, how to monitor costs, and how to make a profit.

Entrepreneurs often calculate product costs as the costs that go into making a product but service costs and administration costs are often ignored as part of the product cost. This creates a skewed idea of how much a product actually costs. Cost allocation methods are designed to allocate costs not necessarily associated with a product, to the appropriate products to get a realistic estimate of costs so that a proper price can be determined for a particular product. The Small Business and Managerial Accounting Training Tutorial offers over seventy lectures designed to give the beginner or new business owner a solid foundation in accounting, and the course includes comprehensive tuition on the various cost accounting systems.

The maintenance department costs, for example, need to be taken into account because you can’t produce a product in a defective building so the maintenance department costs are actually a part of the price of producing the product. The same can be said for the costs of the human resources department for example. Proper cost allocation is essential to get a realistic idea of profit and loss. For a brief overview of profit and loss, check out this Sample Profit and Loss Statement and its usage blog.

In order to make provision for these costs, various tools and methods have been developed to allocate costs appropriately within the organization. Cost allocation methods include:

· The direct method of cost allocation

· The step down method of cost allocation

To illustrate how these cost allocations work, we will use the following example:

An organization manufactures two different products, namely product A and product B. The organization also has an HR department in charge of staff recruitment and a maintenance department in charge of machines and general maintenance. We need to allocate the costs of the various departments to the production of product A and Product B so that we can calculate an accurate sales price that includes sufficient profit.

The Direct Method of Cost Allocation

The direct method of cost allocation is the most popular method used for allocating costs. This method allocates all the service department costs to the production department and does not take into account that the service department offers services to other departments.

Using the example given above, let us assume that the HR department hired 3 staff members for product A and 7 staff members for product B. Using the direct cost method, all costs are directly associated with each product. The cost allocation would be as follows:

Cost of HR department: $ 10,000.00

Using the direct method, 30% of the HR cost will be assigned to Product A and 70% of the costs will be allocated to product B:

Allocation of costs to Product A: 30% of $10,000.00 = $ 3,000.00

Allocation of costs to Product B: 70% of $10,000.00 = $ 7,000.00

The direct method does not take into account the fact that the various service departments actually offer services to one another. The HR department for example is responsible for hiring staff for the maintenance department and the maintenance department also maintains the HR department’s equipment.

The ChalkTalk: Financial Accounting course from Udemy uses various images and drawings to help you to understand how accounting really works. It offers over a hundred lectures and three hours of video content that are aimed at ensuring you understand how the basic accounting principles work.

The Step Down Method of Cost Allocation

The step down method takes into account that certain costs are incurred by the HR and maintenance department. The step down method ranks the service departments in terms of service importance and then uses various steps to allocate the costs to the various products involved.

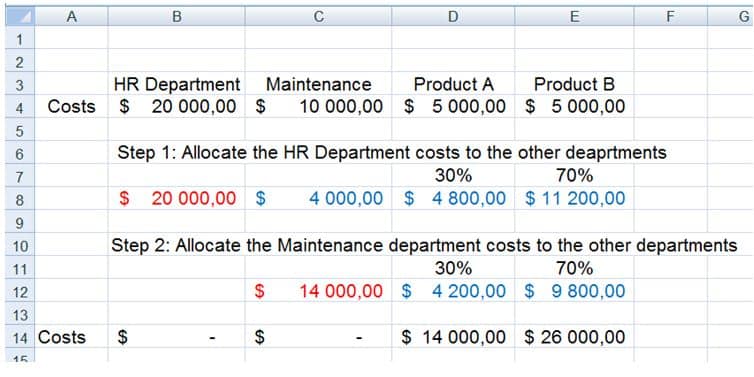

For the purposes of our example, we will rank the HR department as the top department and the maintenance department as the second department. We have set up a spreadsheet to show the costs and various steps involved in the step down allocation method:

The step down method starts with the costs involved for each department. In this case the HR department costs are $20 000.00, the maintenance department costs are $10 000.00, and the direct costs involved in Product A and Product B are $5000.00 each. We start by allocating the HR department costs to all of the other departments using percentages for each department. Now the maintenance depart has $ 14 000.00 worth of costs to allocate. In the next step we allocate the maintenance department costs to each product according to the percentage used. We continue this step down method until all the costs have been allocated to the products.

The step down method of cost allocation is a little more complicated than the direct method of cost allocation, but the results are more accurate in terms of cost allocation.

Cost Allocation Affects Your Bottom Line

There are numerous other cost allocation methods, but the above two methods are the most popular and most well used within industry. It is however important to make sure that the method you use reflects the actual costs of your products to ensure your company’s profits and its ultimate survival.

If you are interested in a career in bookkeeping, then the Introduction to Bookkeeping (Accounting) course offers comprehensive training, including an introduction to bookkeeping as well as training on the various aspects of cost and cost classification.